The Retirement Planning Questions You Should Not Ignore After 60

After 60, retirement starts to feel more real.

You may be thinking about when to stop working, when to claim Social Security, how much income you will need, how to use savings, whether your home still fits your life, and what healthcare may cost in the years ahead.

These questions can feel overwhelming, especially when they are all connected.

But ignoring them usually creates more stress later.

The goal is not to have every answer today. The goal is to start asking the right questions so you can make decisions with more clarity, confidence, and peace of mind.

Why Questions Matter After 60

Retirement planning after 60 is not only about numbers.

It is about understanding how your money supports your real life.

The right questions can help you review:

- Monthly income

- Social Security timing

- Savings withdrawals

- Healthcare costs

- Housing decisions

- Family responsibilities

- Emergency planning

- Important documents

- Long-term stability

Asking questions early gives you more time to adjust before decisions become urgent.

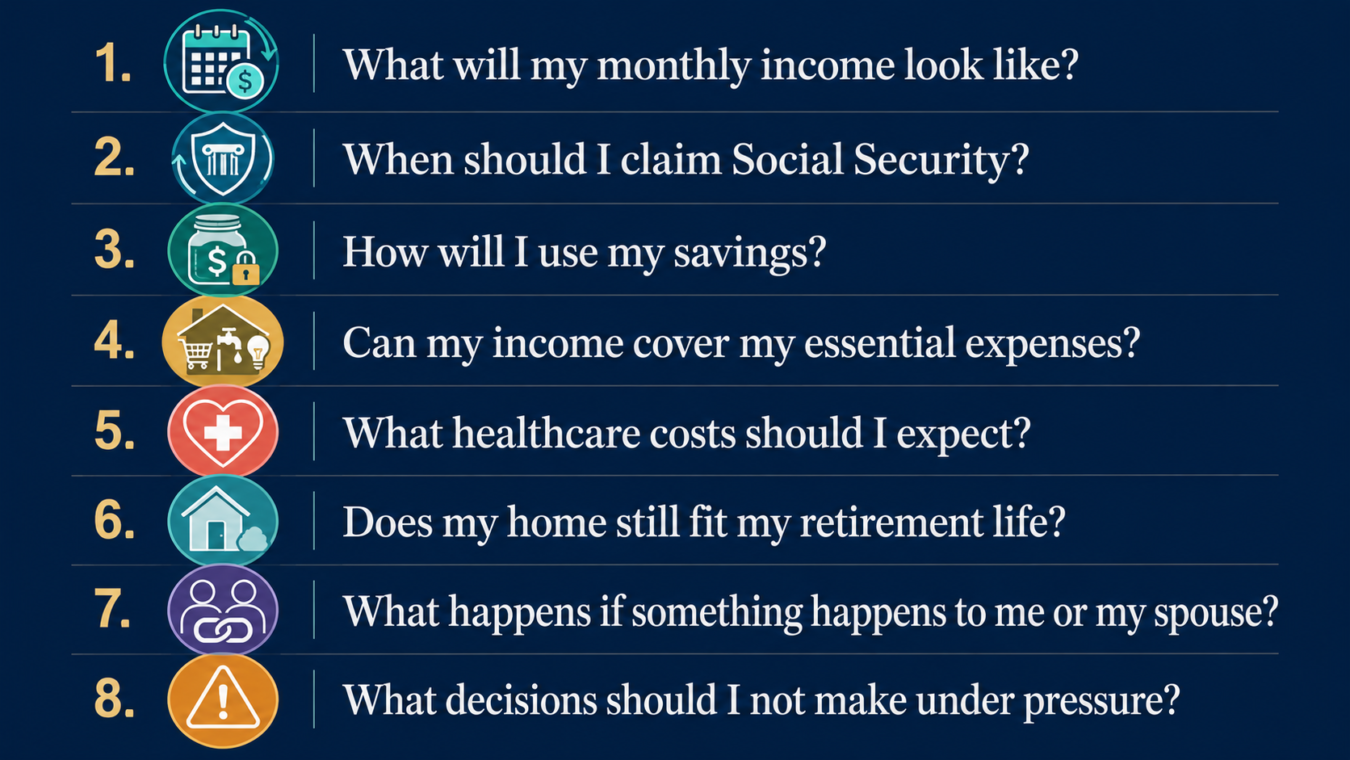

Question 1: What Will My Monthly Income Look Like?

One of the most important retirement questions is:

How much income can I count on every month?

Your income may come from:

- Social Security

- Pension benefits

- Retirement account withdrawals

- Personal savings

- Annuities

- Rental income

- Part-time work

- Other recurring income

Instead of only focusing on total savings, look at monthly support.

Ask:

- Which income sources are reliable?

- Which income sources may change?

- How much will come in each month?

- Will this income support my essential expenses?

- Would my spouse or loved one understand the income plan?

A clear monthly income picture can reduce uncertainty.

Question 2: When Should I Claim Social Security?

Social Security is a major decision for many retirees.

The timing can affect your monthly benefit and may also affect your household’s long-term income.

Before deciding, ask:

- Do I need income right away?

- Am I still working?

- What are my essential expenses?

- Do I have other income sources?

- How is my health?

- How would this decision affect my spouse or survivor income?

- Do I understand the tradeoffs?

There is no single answer that works for everyone.

The best Social Security decision depends on your full retirement picture.

Question 3: How Will I Use My Savings?

Savings can provide flexibility in retirement, but they should be used with purpose.

Ask:

- How much will I withdraw each month?

- Are withdrawals planned or reactive?

- Am I using savings for essentials or lifestyle expenses?

- How long may savings need to last?

- Am I protecting an emergency cushion?

- Could healthcare or housing costs increase withdrawals later?

Your savings are not just a balance. They are part of your future stability.

Question 4: Can My Income Cover My Essential Expenses?

Essential expenses should be reviewed before lifestyle spending.

These may include:

- Housing

- Utilities

- Groceries

- Transportation

- Healthcare

- Prescriptions

- Insurance

- Taxes

- Debt payments

- Home maintenance

Ask:

Can my reliable income cover these needs?

If the answer is no, it does not mean failure. It means the plan needs attention.

You may need to review expenses, income sources, housing costs, savings withdrawals, or part-time income options.

Question 5: What Healthcare Costs Should I Expect?

Healthcare should never be treated as an afterthought in retirement planning.

Even with Medicare, you may still have costs such as:

- Premiums

- Deductibles

- Copays

- Prescription drugs

- Dental care

- Vision care

- Hearing care

- Medical equipment

- Transportation to appointments

Ask:

- Are my prescriptions affordable?

- Do I understand my coverage?

- Could my healthcare needs change?

- Do I have money set aside for medical surprises?

- Could healthcare affect where I live or how much support I need?

Healthcare planning is part of financial planning.

Question 6: Does My Home Still Fit My Retirement Life?

Your home can provide comfort, memories, and stability. But it can also become expensive or difficult to maintain.

After 60, ask:

- Is my home still affordable?

- Are property taxes, insurance, utilities, or repairs increasing?

- Is the home safe and accessible?

- Are stairs or maintenance becoming a concern?

- Am I close to doctors, stores, transportation, and family support?

- Would downsizing or relocating reduce pressure?

- Would staying require home modifications?

The right housing decision is not only financial. It should support your health, independence, lifestyle, and peace of mind.

Question 7: What Happens If Something Happens to Me or My Spouse?

This question is uncomfortable, but important.

Retirement planning should protect the people you love.

Ask:

- Would income change if one spouse passes away?

- Would Social Security or pension income continue?

- Are beneficiaries updated?

- Are important accounts organized?

- Does someone trusted know where documents are kept?

- Are emergency contacts current?

- Do loved ones understand your wishes?

Planning ahead can reduce confusion during emotional moments.

Question 8: What Decisions Should I Not Make Under Pressure?

After 60, you may receive advice, offers, or recommendations about money, insurance, investments, housing, or benefits.

Before acting, ask:

- Do I understand this clearly?

- What are the risks?

- What are the costs?

- What happens if I wait?

- Why am I being asked to decide quickly?

- Have I reviewed this with someone I trust?

Be cautious if someone says:

- “You must decide today.”

- “There is no risk.”

- “This is guaranteed.”

- “Do not ask anyone else.”

- “Everyone your age should do this.”

A good decision should allow time for questions.

Final Thoughts

The retirement planning questions you should not ignore after 60 are the ones that affect your income, healthcare, housing, savings, family protection, and peace of mind.

You do not need to solve everything at once. Start with one question. Then review the next. Step by step, uncertainty becomes clarity.

At EduFuture Foundation, we believe retirement education should be clear, practical, respectful, and pressure-free. Our mission is to help older adults and families understand retirement decisions so they can move forward with confidence, dignity, and peace of mind.

To learn more about our educational programs, seminars, and financial counseling resources, visit edufuturefoundation.org.